New Earth Track analysis shines a light on fossil fuel subsidies through tax-exempt master limited partnerships (MLPs)

If a company or an industry is going to get subsidized, there are good ways and there are better ways for it to happen if one is sitting in the corporate suite. Among the best is to receive big subsidies that, while not flowing to your competitors, arrive in a form that nobody seems to notice. The benefits of this structure are clear: while the recipient gets a large slug of financial support, because few people see or understand the largesse, the political cost to both obtain and retain the subsidy is relatively low. Master Limited Partnerships, the subject of Earth Track's most recent report Too Big to Ignore: Subsidies to Fossil Fuel Master Limited Partnerships, prepared for Oil Change International, fit the bill here perfectly:

- They are big. Not only can beneficiary companies with hundreds of billions of dollars in market cap entirely escape corporate income taxes on profits earned from eligible activities, but they can also defer for many years any tax payments on the gobs of cash they distribute out to their owners.

- They are mostly hidden. Energy subsidy studies documenting tax breaks conducted in recent years by the US Department of Energy, the Congressional Budget Office, the US Treasury, and the Government Accountability Office have either not mentioned MLP subsidies at all, or done so only in passing with no related numerical estimate. The Congressional Research Service did mention the tax break, but did not link it to energy. Only the Joint Committee on Taxation (JCT) both linked the tax break to energy and included an estimated revenue loss figure. Unfortunately, JCT's first estimates came only in 2008, though fossil fuel MLPs were already surging in earlier years.

- They are selective. Because most industries can't partake in this little game, the tax exemption for MLPs generates an especially big market boost to oil and gas over other energy options. Nearly every other industry lost their ability to form tax-favored publicly-traded partnerships like MLPs in 1987, more than a quarter-century ago. The reason? Congress was afraid corporate income tax revenues would be gutted. Since that time, fossil fuels have increasingly dominated this tax break, comprising well more than 75% of the sector by 2012.

- They have (until this point) little political risk. Fossil fuel MLPs continue to grow very quickly, and, unlike common and highly visible subsidies to wind and solar, MLP tax breaks never expire.

Selective Subsidies That Work Counter to National Fiscal and Environmental Goals

- MLP tax expenditures are part of a broader set of government subsidies that continue to underwrite activities contributing to climate change. These policies not only have large fiscal costs, but also work counter to the country's environmental goals and our national interest.

- Fossil fuel MLPs are growing quickly. The market capitalization of fossil fuel MLPs reached an estimated $385 billion by the end of March 2013, up from less than $14 billion in 2000. Related tax subsidies have been as high as $4 billion annually in recent years at the federal level alone. Because the tax benefits from MLPs also ripple through state income tax codes, the combined state and federal MLP subsidies would be even higher.

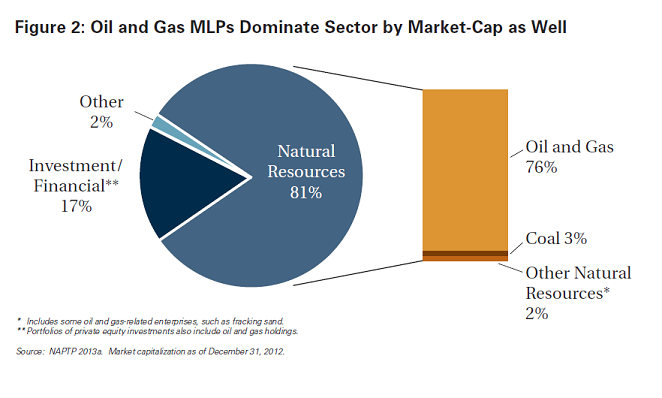

- Fossil fuel activities continue to dominate MLPs, both in number of firms and share of total market capitalization. As of the end of last year, 77 percent of MLPs were in the oil, gas, and coal sectors based on data collected by the National Association of Publicly Traded Partnerships (NAPTP), the main industry trade association. Firms in the fossil fuel sectors comprised 79 percent of total MLP market capitalization, though this figure is likely a bit low. Firms classified in other sectors also include some oil and gas-related businesses, including fracking sand and fossil fuel investments held by publicly-traded private equity firms such as Blackstone.

MLP Subsidies to Fossil Fuels: Underestimated and Ignored for Too Long

- Government estimates of tax expenditures from energy-related MLPs are too low. Tax expenditures related to MLPs have been understated in recent years, and appear to be growing rapidly. Using a variety of estimation approaches, we estimate that tax preferences for fossil fuel MLPs cost the Treasury as much as $13 billion over the 2009-12 period, more than six times the official estimates.

- MLP tax breaks are among the largest subsidies to fossil fuels. Although most government reviews of energy subsidies have not even included MLP-related tax expenditures, our estimates suggest this subsidy is among the top five largest fiscal subsidies to the fossil fuel sector and the largest single tax break to the sector.

- Growing share of production cycle for oil, gas, and coal can be organized as a tax-favored MLP - indicative that revenue losses will continue to grow. Financial innovation and IRS private letter rulings have expanded the fossil fuel market segments able to legally and successfully operate as tax-favored MLPs. Recent innovations have even established a precedent by which MLPs have successfully acquired taxable corporations, taking them off the corporate tax role in the process.

MLPs for All? Providing Matching Tax Breaks to Renewables May Not be a Panacea

Though supported by many environmental groups, recent legislation introduced to expand MLP-eligibility to a range of new energy technologies may not be the panacea it is widely believed to be by supporters. Further, the legislation is currently worded to include a range of energy technologies such as waste-to-energy, landfill gas, coal-to-liquids, and biomass that have a decidedly mixed environmental profile.

Even in well-established market segments, there is a large overhang of fossil fuel assets poised to exit the corporate income tax system through conversion to MLPs. Less than 20 percent of total assets in the refiners, exploration and production, oil services, and coal sectors are presently held in a tax-favored MLP format (see Table). Even in the MLP-intensive midstream segment of the oil and gas market, conventional (taxable) corporate forms continue to own more than half of the assets. In all of these sectors, there is a huge pool of assets that multiple investment firms anticipate will convert to MLPs in coming years.

Even in well-established market segments, there is a large overhang of fossil fuel assets poised to exit the corporate income tax system through conversion to MLPs. Less than 20 percent of total assets in the refiners, exploration and production, oil services, and coal sectors are presently held in a tax-favored MLP format (see Table). Even in the MLP-intensive midstream segment of the oil and gas market, conventional (taxable) corporate forms continue to own more than half of the assets. In all of these sectors, there is a huge pool of assets that multiple investment firms anticipate will convert to MLPs in coming years.

- Proposed expansion of MLP eligibility to renewables risks disproportionate benefits flowing instead to the fossil fuel sector. Current efforts to expand MLP treatment to renewables (The Master Limited Partnerships Parity Act) may entrench existing subsidy recipients. The expansion will reduce the likelihood that MLP's tax-exempt treatment will be ended for fossil fuel producers, allowing the rapid growth of tax-exempt fossil fuel MLPs to continue unchecked. This legislation also would open MLP-eligibility to power generation for the first time, creating risks that this treatment will be extended from the current proposed set of recipients (biomass, solar, wind, geothermal) to all forms of power generation in coming years. This would disadvantage energy conservation, offset hoped for gains from the expansion in renewable sectors, and trigger very large tax losses to Treasury.

MLP Subsidy Termination a More Logical Path than Further Expansion

The MLP loophole should be closed; MLPs should be taxed as conventional corporations, not extended to new uses. This strategy, continuing what the United States started in 1986, would eliminate large and growing subsidies to fossil fuels. Canada also successfully ended tax-favored treatment of an equivalent corporate structure in 2006. In both cases, the affected industries did not wither and die; they adapted and moved on. This newest crop of tax-favored fossil fuel firms will do the same.